PERSPECTIVES #12

Energy transition, electrification and robotization: a single industrial logic

Télécharger l’intégralité du document en PDFThe energy transition is often described as a decarbonization challenge, framed around emissions reduction targets and fuel substitution pathways. While this framing is necessary from a policy perspective, it remains insufficient to explain the industrial reality of the transition. What is unfolding is not merely a cleaner energy system, but a re-engineering of industrial production systems, driven by the replacement of thermal constraints with electrical and digital ones.

Historically, industrial value creation has been shaped by thermodynamics. Combustion based energy systems imposed constraints in the form of inertia, ramping limitations, heat transfer losses and mechanical coupling. These constraints defined plant layouts, production rhythms and economies of scale. Electrification progressively relaxes these constraints.

This paper aims to underline that the energy transition therefore does not simply coexist with robotization; it creates the technical and economic conditions for its large-scale deployment. Energy transition is actually the interliage between clean energy deployment, electrification and robotization.

The rise of electricity as the main source of energy

Electricity can increasingly be transported with low losses, converted into motion or heat with high efficiency, and — critically — controlled at very fine time scales, explaining the inexorable rise of electricity in useful energy supply since a century.

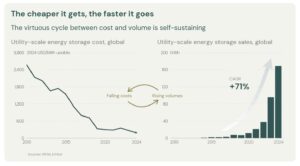

The major challenge to electricity being widely used in industrial processes was the inability to store it efficiently. This feature changed with the industrialization of Lithium-ion batteries, driven primarily by the automotive sector. The dramatic drop in Electric Vehicles storage costs triggered a drop in utility-scale storage costs, enabling a fast deployment of Battery-Energy Storage Systems (BESS), changing fundamentally the electricity equation by enabling MW-scale storage.

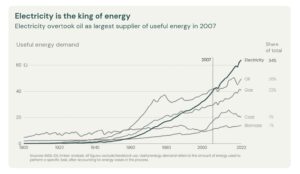

It is hence striking to see that electricity surpassed oil as the main source of useful energy in the world in 2007, the year considered for the kick-off of the shale revolution in the US. Eventually, despite the US becoming a net exporter of oil and the largest exporter of LNG due to this revolution, the inexorable decrease in and storage costs propelled electricity as the number 1 source of useful energy.

This movement only accelerated a trend that has been at play for about 40 years in various sectors: because of its inherent qualities compared to thermodynamic cylces (higher yields, lower losses, easier power management, modularity, etc.), electricity is preferred every time possible, through all industries. The two main sectors where electricity was marginal were sectors using high temperature industrial heat (cement, steel and metals, pulp and paper, etc.) and transportation. Regarding the latter, road transportation alone consumes roughly 35% of global oil production.

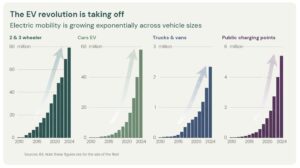

As EV adoption is set to be a defining trend of the energy and industrial landscape of this century, it will likely further accelerate the electrification of the overall economic system and hence the need for electricity.

This accelerating trend of electrification has a major consequence for an industrial processes perspective: it fundamentally alters the conditions under which automation and robotization become viable.

Robotization and the reshaping of industrial electricity demand

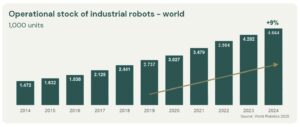

Global deployment figures illustrate the scale of this transformation. According to the International Federation of Robotics, annual installations of industrial robots increased from roughly 250,000 units in 2014 to over 540,000 units in 2024, while the global operational stock reached approximately 4.7 million robots. Projections indicate installations approaching 700,000 units per year by 2028, with cumulative stock continuing to rise accordingly.

Beyond the deployment of industrial robots, the last five years have been marked by the increasing deployment of collaborative industrial robots (or cobots), with a 60% increase between 2020 and 2021 and a subsequent 40% increase from 2021 to 2022 according to the International Federation of Robotics.

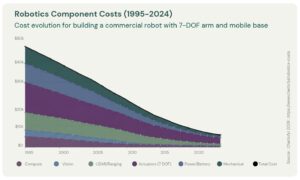

A key driver of this accelerated adoption is the dramatic decrease in robotic components costs coupled with enhanced performance. The chart below shows that between 1995 and 2024, the cost of key robotic components decrease by nearly 90%. The most pronounced decrease is linked to powering the robots, in particular the batteries.

Equally important if not more is the progress made in robots integration in industrial processes. The TCO of a robot is derived from the cost of the hardware (the robot itself), the ease of integration and of programming and the maintenance. Programming (no-code / low code), integration (plug & play cobots) have in decreased particularly sharply over the last years, enabling a much faster adoption.

Performance has also improved significantly, driven by three major collateral technological evolutions : 1) vision (cameras, objects recognition through deep learning), 2) flexibility (multi-task cobots, fast reprogramming) and 3) intelligence driven by software and AI integration (learning by demonstration and real time adaptation).

Electrification as the enabling layer of automation

Another fundamental shift is that modern Industrial robots and cobots are electric-native assets, using electricity to replace other energy vectors: less compressed air, less hydraulic oil, less auxiliary thermal energy. Electricity becomes more granular and controllable as robots can be stopped, slowed, rescheduled, energy use hence aligns more closely with production output. This is very different from furnaces, boilers, steam networks, which are slow, inertial, and difficult to modulate.

Industrial robots are not energy-intensive assets in isolation. A typical articulated industrial robot consumes on the order of 5–10 MWh per year, depending on payload and duty cycle — modest when compared to furnaces, compressors or chemical reactors. The relevance of robotization for electricity demand lies elsewhere.

Robots are electric-native capital goods. They require stable power quality, fast response times and tight integration with electronic control systems. The same is true for Computer Numerical Control (CNC) machines, automated conveyors, robotic welding systems, pick-and-place units and automated storage and retrieval systems. As a result, factories that automate tend to restructure their entire energy architecture around electric drives, variable-speed motors, power electronics and digital control layers.

This shift is visible in equipment-level statistics. According to the IEA-EMSA platform [1], electric motors already account for roughly 50% of global electricity consumption, and more than 70% of industrial electricity use. Automation increases both the number of motors per unit of output and the degree to which they are actively controlled rather than run at constant load. Variable-speed drives, servo motors and electronically controlled actuators become the norm.

The implication is that automation does not merely add electric loads; it converts previously thermal or mechanical processes into actively controlled electric ones. This is a qualitative change in electricity demand.

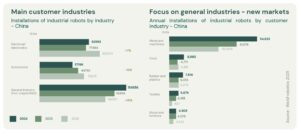

It is also key to look at where robots are being deployed. While the automotive sector remains a major user, it is no longer the primary driver of incremental growth. “General industries” — metals, machinery, plastics, chemicals, food and other process industries — now account for an increasing share of new installations. These sectors are typically characterized by:

- higher energy intensity,

- greater reliance on thermal processes,

- and historically lower levels of automation.

As robots diffuse into these sectors, automation and electrification advance together. Automated production lines rely on electric drives, sensors and control systems, while utilities — compressed air, pumping, heating — are increasingly electrified and optimized digitally. Electricity demand grows, but more importantly, it becomes more granular, more responsive and also and. It is also worth noting the cobots are disproportionately deployed in sectors that are traditionally energy-intensive, rely heavily on process heat and have therefore low automation rate until now, such as food & beverages, packaging, plastics, but also in the wider space of SMEs and midcaps.

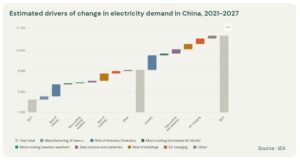

China illustrates this linkage between energy transition and industry. While the current debate on energy – in the US, but also in Europe, focuses on supplying power to datacenter of the AI revolution and the “hyperscalers’” ambition in that field, the foreseen evolution of the Chinese mix tells a very different story: between 2024 and 2027, the IEA foresees an increase of 1800 TWh of electricity demand. While datacenters account for 200 TWh of additional demand (slightly less that Spain’s entire electricity demand), Industry accounts for over 800 TWh (or the electricity demand of Germany and Italy combined).

The underestimated role of process heat electrification

The most significant leverage effect lies in industrial process heat, which accounts for approximately two thirds of final industrial energy consumption globally. Today, the vast majority of this heat is supplied by fossil fuels. Electricity represents less than 5% of final energy used for process heat and steam [2].

This low starting point creates the illusion that the potential for electrification of heat is marginal. In reality, it represents one of the largest sources of future electricity demand growth. High-electrification scenarios consistently show electricity use for industrial heat increasing by a factor of four to five, eventually accounting for 25–35% of total industrial heat demand, depending on region and sector.

Automation plays a decisive role in making this transition feasible. Electrified heat technologies — electric boilers, induction heating, infrared systems and industrial heat pumps — integrate far more effectively into digitally controlled production environments than combustion-based systems. Once production is automated, electrifying heat becomes an extension of the same logic: precise control, fast response, reduced losses and easier integration into optimization loops.

Efficiency reinforces this trend. For low- and medium-temperature applications (which represent a substantial share of industrial heat demand), industrial heat pumps routinely deliver three to four units of usable heat per unit of electricity, compared to gas boilers operating at 80–90% efficiency. Automation ensures that these systems operate close to optimal conditions, further improving effective performance.

Automation, flexibility and power system constraints

As electricity systems decarbonize, flexibility becomes a binding constraint. Variable renewable generation increases the value of demand that can adjust in response to system conditions. Automation is a prerequisite for this flexibility.

Manually operated, thermally constrained processes are difficult to modulate without significant productivity losses. Automated, electrically driven processes can be ramped, paused or rescheduled with much lower marginal cost. This is particularly relevant in sectors where robots handle discrete tasks — machining, assembly, packaging — but also increasingly in continuous processes as advanced control systems are deployed.

The result is that robotized factories are not only more productive, but structurally better suited to operate within constrained, low-carbon power systems. Their electricity demand can be shaped through pricing, contracts and digital control, turning industrial loads into system assets rather than liabilities.

This transformation also feeds back into investment decisions. Grid operators, utilities and policymakers increasingly recognize that electrified, automated industry can play a role in balancing power systems. This recognition further strengthens the economic case for electrification and automation, reinforcing the flywheel. Taken together, these elements form a cumulative dynamic:

This dynamic explains why electrification, robotization and the energy transition advance together across regions and sectors, rather than sequentially. It also explains why attempts to analyze them in isolation consistently underestimate their impact.

Implications for industrial strategy and investment

For industrial players, the implication is that competitiveness increasingly depends on the coherence of energy, automation and digital strategies, rather than on any single lever. For investors, value creation lies at the intersections: power electronics, automation platforms, electrified process equipment, industrial software and system integration. Energy is a sector that drives all other sectors, either due to cost, reliability or security of supply.

It of course has a particular implication from a sovereignty perspective. China has famously surpassed a 1tn USD global trade surplus in 2025, drawing reactions from all over the world, mostly from the G7 nations. According to the CEPR, its share in manufacturing has increased from 5% of the world gross output in 1995 to over 35% in the 2020s.

This inexorable rise of Chinese industrial power can be put in parallel of two underlying trends:

For industrial players, the implication is that competitiveness increasingly depends on the coherence of energy, automation and digital strategies, rather than on any single lever. For investors, value creation lies at the intersections: power electronics, automation platforms, electrified process equipment, industrial software and system integration. Energy is a sector that drives all other sectors, either due to cost, reliability or security of supply.

It of course has a particular implication from a sovereignty perspective. China has famously surpassed a 1tn USD global trade surplus in 2025, drawing reactions from all over the world, mostly from the G7 nations. According to the CEPR, its share in manufacturing has increased from 5% of the world gross output in 1995 to over 35% in the 2020s.

This inexorable rise of Chinese industrial power can be put in parallel of two underlying trends:

For industrial players, the implication is that competitiveness increasingly depends on the coherence of energy, automation and digital strategies, rather than on any single lever. For investors, value creation lies at the intersections: power electronics, automation platforms, electrified process equipment, industrial software and system integration. Energy is a sector that drives all other sectors, either due to cost, reliability or security of supply.

It of course has a particular implication from a sovereignty perspective. China has famously surpassed a 1tn USD global trade surplus in 2025, drawing reactions from all over the world, mostly from the G7 nations. According to the CEPR, its share in manufacturing has increased from 5% of the world gross output in 1995 to over 35% in the 2020s.

This inexorable rise of Chinese industrial power can be put in parallel of two underlying trends:

- it is well known that China is the arch-dominant player in cleantechs and clean energy. In 2024, 60% of all solar PV capacity was installed in China, and China controls between 60% and 90% of key cleantechs.

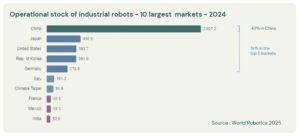

- Less known maybe is the pace at which China is automating its industry and the advance it has taken on all other major industrial nations, with the possible exception of South Korea and Japan. The IFR report shows that in 2024, 43% of all industrial robots were installed in China.

The energy transition is therefore not only about cleaner energy. It is about different factories, operating under different constraints, with different economics. Robotization is not a side effect of this transition; it is one of its core transmission mechanisms. And focusing on the sole dimension of energy production and energy management is running the risk of falling behind industrially and hence economically.

The implications for European SMEs and midcaps are existential: whereas well designed regulations and policies should shield them from unfair Chinese (or US as the case may be) competition, they cannot ignore the fact that the lack of automation and the reduced pace of the energy transition will translate into a structural deficit of competitiveness.

[1] https://www.iea-4e.org/emsa/

[2] https://www.iea.org/reports/renewables-2025/renewable-heat